Portability Election for Estates and Trusts - 4 Alternative Clauses (3 Pages)

This Form provides alternative Portability Clauses to be used in connection with a Will or Trust. The concept of Portability was introduced in the 2010 Tax Relief Act (as new Code Section 2010 (c)) as a way to permit an election to be made for the unused federal estate tax exemption of a decedent to pass to his or her surviving spouse so the spouse could utilize the exemption. The Portability rules introduce a new phrase into the estate planning lexicon, the “deceased spousal unused exemption” (DSUE) which will be used in the Forms suggested below.

Even with the enhanced transfer tax exemption of the 2017 Tax Cuts and Jobs Act, filing Form 706 to gain portability remains the tax planner’s recommendation. The 2017 Act sunsets after 2025. “Political risk” suggests that the current exemption could be reduced sooner. View the portability election as “death tax insurance” – just in case the surviving spouse of a modest estate suddenly and unexpectedly becomes wealthy, the enhanced DSUE from the deceased spouse is in place.

This Form provides alternative Portability Clauses to be used in connection with a Will or Trust. The concept of Portability was introduced in the 2010 Tax Relief Act (as new Code Section 2010 (c)) as a way to permit an election to be made for the unused federal estate tax exemption of a decedent to pass to his or her surviving spouse so the spouse could utilize the exemption. The Portability rules introduce a new phrase into the estate planning lexicon, the “deceased spousal unused exemption” (DSUE) which will be used in the Forms suggested below.

Even with the enhanced transfer tax exemption of the 2017 Tax Cuts and Jobs Act, filing Form 706 to gain portability remains the tax planner’s recommendation. The 2017 Act sunsets after 2025. “Political risk” suggests that the current exemption could be reduced sooner. View the portability election as “death tax insurance” – just in case the surviving spouse of a modest estate suddenly and unexpectedly becomes wealthy, the enhanced DSUE from the deceased spouse is in place.

Portability was made permanent by the American Tax Relief Act of 2012 (ATRA). The IRS has recently issued guidance requiring that in order to elect Portability, the executor of the decedent’s estate must file a timely and complete federal estate tax return. The filing of the return, absent an affirmative election out of the Portability election on the filed return, is deemed a making of the Portability election. Failure to file Form 706 will result in a denial of the Portability opportunity. The IRS has granted taxpayers two years from a decedent’s date of death to file Form 706 for purposes of portability. Filings delayed beyond two years will require a private letter ruling application and the payment of a $10,000 user fee.

In many cases, Portability will be favored to insure use of the maximum federal transfer tax exemptions for both spouses of a marriage. In rare cases, it will not be favored, either because other planning techniques are preferred (such as a full funding of the available applicable exclusion at the death of the first spouse to die) or as the result of a desire to deny the surviving spouse the use of the decedent’s unused exclusion for further transfers.

At the present time, Portability is only allowed with respect to the federal estate tax exemption, and not that of any state. However, in the event the Portability concept is adopted by a state, the language of the Forms below allows for a state Portability election as well.

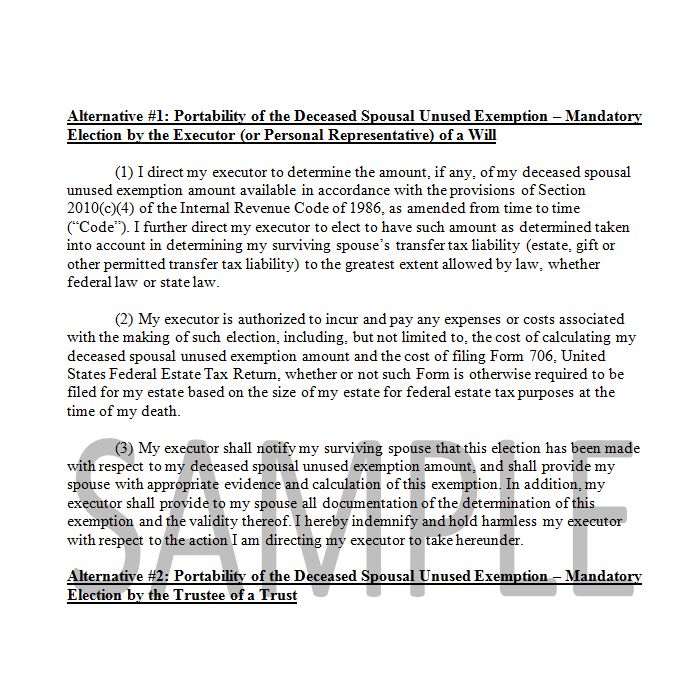

Alternative #1 provides for the mandatory election of portability by the executor of the decedent’s estate.

Alternative #2 addresses the possibility that no executor is appointed for the estate (such as where the entire estate plan of the decedent is contained in a revocable trust) and then the trustee is directed to make the portability election.

Alternative #3 gives the executor the discretion to make the portability election.

Alternative #4 gives the trustee the discretion to make the portability election.

Author:

Steven G. Siegel is president of The Siegel Group, a Morristown, New Jersey - based national consulting firm specializing in tax consulting, estate planning and advising family business owners and entrepreneurs. Mr. Siegel holds a BS from Georgetown University, a JD from Harvard Law School and an LLM in Taxation from New York University.

He is the author of several books, including: Planning for An Aging Population; Business Entities: Start to Finish; Taxation of Divorce and Separation; Income Taxation of Estates and Trusts, Preparing the Audit-Proof Federal Estate Tax Return, Putting It Together: Planning Estates for $5 million and Less, Family Business Succession Planning, Business Acquisitions: Representing Buyers and Sellers in the Sale of a Business; Dynasty Trusts; Planning with Intentionally-Defective Grantor Trusts; The Federal Gift Tax: A Comprehensive Analysis; Charitable Remainder Trusts, Grantor Trust Planning: QPRTs, GRATs and SCINs, The Estate Planning Course, The Retirement Planning Course, Retirement Distributions: Estate and Tax Planning Strategies; The Estate Administration Course, Tax Strategies for Closely-Held Businesses, and Tort Litigation Settlements: Tax and Financial Issues.

Mr. Siegel has lectured extensively throughout the United States on tax, business and estate planning topics on behalf of numerous organizations, including National Law Foundation, AICPA, CCH, National Tax Institute, National Society of Accountants, and many others. He has served as an adjunct professor of law at Seton Hall and Rutgers University law schools.

The Siegel Group provides consulting services to accountants, attorneys, financial planners and life insurance professionals to assist them with the tax, estate and business planning and compliance issues confronting their clients. Based in Morristown, New Jersey, the Group has provided services throughout the United States. The Siegel Group does not sell any products. It is an entirely fee-based organization.

Contact the Siegel Group through its president, Steven G. Siegel, e-mail: [email protected].

-

3 Irrevocable Life Insurance Trusts (75 Pages)Special Price $199.00 Regular Price $237.00

3 Irrevocable Life Insurance Trusts (75 Pages)Special Price $199.00 Regular Price $237.00

-

12 Will Forms (168 Pages)$159.00

-

3 Irrevocable Life Insurance Trusts (75 Pages)Special Price $199.00 Regular Price $237.00