GRIT (Grantor Retained Income Trust) (8 Pages)

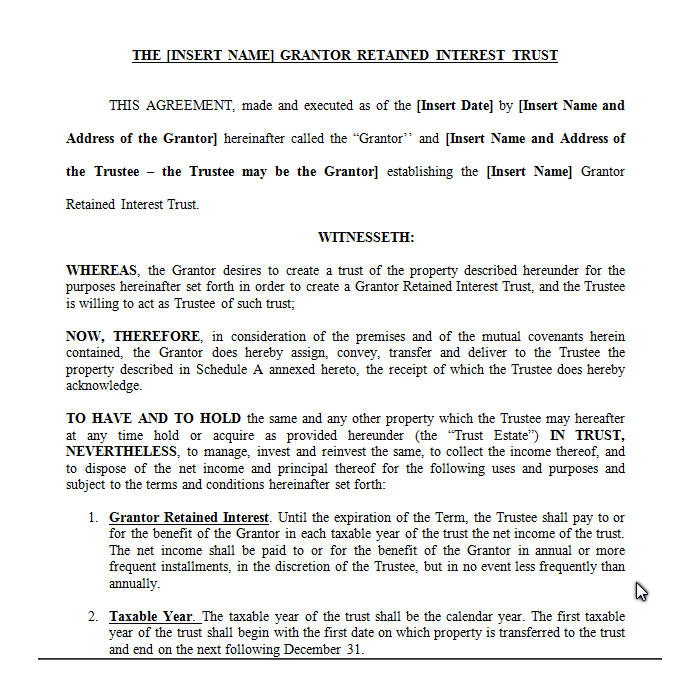

This is a Form of a Grantor Retained Interest Trust (GRIT). It is designed to be in compliance with the rules of Code Section 2702 and the Regulations thereunder. Code Section 2702 provides that a GRIT may not be used for the benefit of “members of the Grantor’s family” as defined in that Section. Accordingly, a GRIT is used for the benefit of persons outside the definition of family members. A GRIT allows the trust Grantor to receive all or as much of the trust income as desired annually for a fixed term.

This is a Form of a Grantor Retained Interest Trust (GRIT). It is designed to be in compliance with the rules of Code Section 2702 and the Regulations thereunder. Code Section 2702 provides that a GRIT may not be used for the benefit of “members of the Grantor’s family” as defined in that Section. Accordingly, a GRIT is used for the benefit of persons outside the definition of family members. A GRIT allows the trust Grantor to receive all or as much of the trust income as desired annually for a fixed term. This is to be distinguished from the Grantor Retained Annuity Trust (GRAT) which provides for a fixed payment to the Grantor from the commencement of the term and from a Grantor Retained Unitrust (GRUT) which provides for a fixed percentage payment to the Grantor of an annually revalued group of assets. The actuarially calculated value of the retained interest by the Grantor in the GRIT is subtracted from the value of the transferred property to determine the amount of the gift for gift tax purposes. The Grantor may provide for outright transfer or transfer into an ongoing trust for beneficiaries at the conclusion of the GRIT term. Death of the Grantor prior to the end of the GRIT term requires the inclusion of the trust property in the Grantor’s estate.

Author:

Steven G. Siegel is president of The Siegel Group, a Morristown, New Jersey - based national consulting firm specializing in tax consulting, estate planning and advising family business owners and entrepreneurs. Mr. Siegel holds a BS from Georgetown University, a JD from Harvard Law School and an LLM in Taxation from New York University.

He is the author of several books, including: Planning for An Aging Population; Business Entities: Start to Finish; Taxation of Divorce and Separation; Income Taxation of Estates and Trusts, Preparing the Audit-Proof Federal Estate Tax Return, Putting It Together: Planning Estates for $5 million and Less, Family Business Succession Planning, Business Acquisitions: Representing Buyers and Sellers in the Sale of a Business; Dynasty Trusts; Planning with Intentionally-Defective Grantor Trusts; The Federal Gift Tax: A Comprehensive Analysis; Charitable Remainder Trusts, Grantor Trust Planning: QPRTs, GRATs and SCINs, The Estate Planning Course, The Retirement Planning Course, Retirement Distributions: Estate and Tax Planning Strategies; The Estate Administration Course, Tax Strategies for Closely-Held Businesses, and Tort Litigation Settlements: Tax and Financial Issues.

Mr. Siegel has lectured extensively throughout the United States on tax, business and estate planning topics on behalf of numerous organizations, including National Law Foundation, AICPA, CCH, National Tax Institute, National Society of Accountants, and many others. He has served as an adjunct professor of law at Seton Hall and Rutgers University law schools.

The Siegel Group provides consulting services to accountants, attorneys, financial planners and life insurance professionals to assist them with the tax, estate and business planning and compliance issues confronting their clients. Based in Morristown, New Jersey, the Group has provided services throughout the United States. The Siegel Group does not sell any products. It is an entirely fee-based organization.

Contact the Siegel Group through its president, Steven G. Siegel, e-mail: [email protected].