Will With Unified Credit Shelter Trust and QTIP Marital Trust With Children's Shares In Trust Until Age 25 (20 Pages)

In stock

SKU

UnifiedCreditShelterTrustandMaritalQTIP

$49.00

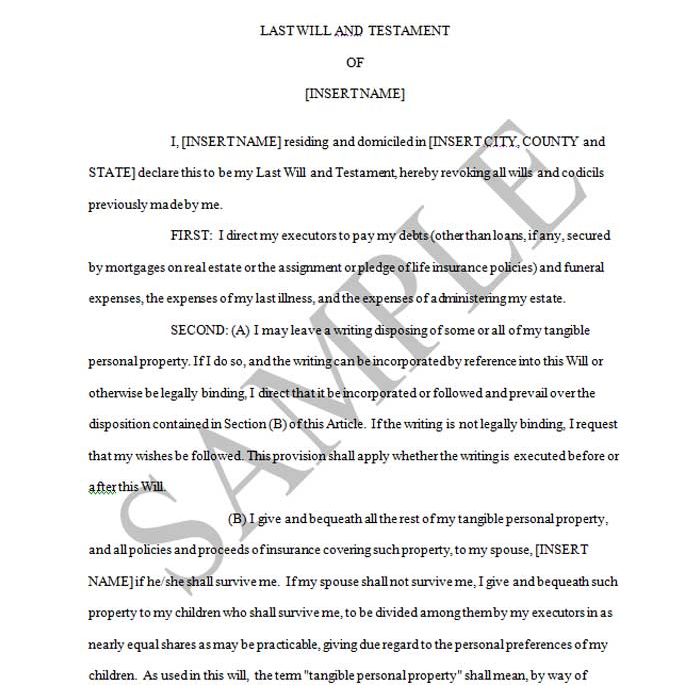

This Will provides for the mandatory creation and funding of a unified credit (aka exemption equivalent trust) (Article Third) for the benefit of the testator’s surviving spouse and children. The balance of the testator’s property passes into a Qualified Terminable Interest Property (QTIP) Trust for the benefit of the surviving spouse.

This Will provides for the mandatory creation and funding of a unified credit (aka exemption equivalent trust) (Article Third) for the benefit of the testator’s surviving spouse and children. The balance of the testator’s property passes into a Qualified Terminable Interest Property (QTIP) Trust for the benefit of the surviving spouse.

Article Third provides that trust income and principal may be distributed in the discretion of the trustee to either the surviving spouse or to the children of the testator. All the income is to be paid annually; the principal is to be paid in the discretion of the trustee, and may be used for health, education, support and maintenance. It is suggested (but not required) that the interests of the surviving spouse are to take precedence in considering distributions.

Article Fourth leaves the balance of the testator’s estate in a QTIP Trust for the exclusive lifetime benefit of the surviving spouse. All of the Trust income is to be paid to the spouse and the spouse is the only permitted beneficiary of principal during his/her lifetime. If there is no surviving spouse, the balance of the testator’s estate passes outright to children, i.e. outright if all have reached age 25, or in trust until the youngest child reaches age 25, as the case may be. (Article Fourth (E)). Similarly, if the spouse survives and the Article Third Trust is created, when the second death of the spouses occurs, the remaining balance of the Article Third trust property passes to children either outright or in trust if age 25 has not yet been reached by the youngest child.

Note the tax allocation clause contained in Article Sixth directing that any taxes or administrative expenses be paid first from the Article Third Trust. This is done to avoid reducing the marital deduction share (Article Fourth) by taxes and expenses, which would correspondingly reduce the marital deduction. Article Sixth also contains provisions permitting the QTIP treatment to be elected by the executor at the death of the testator. Note also in Article Sixth the discretion given the fiduciaries to address a possible generation-skipping problem by allowing the fiduciaries to take all necessary steps to avoid generation-skipping tax liability should this issue arise.

The order of deaths in Article Ninth (smaller estate holder deemed to be the survivor) is included to attempt to achieve the optimal use of the exemption equivalent in each spouse’s estates in the event of a simultaneous death.

Author:

Steven G. Siegel is president of The Siegel Group, a Morristown, New Jersey - based national consulting firm specializing in tax consulting, estate planning and advising family business owners and entrepreneurs. Mr. Siegel holds a BS from Georgetown University, a JD from Harvard Law School and an LLM in Taxation from New York University.

The order of deaths in Article Ninth (smaller estate holder deemed to be the survivor) is included to attempt to achieve the optimal use of the exemption equivalent in each spouse’s estates in the event of a simultaneous death.

Author:

Steven G. Siegel is president of The Siegel Group, a Morristown, New Jersey - based national consulting firm specializing in tax consulting, estate planning and advising family business owners and entrepreneurs. Mr. Siegel holds a BS from Georgetown University, a JD from Harvard Law School and an LLM in Taxation from New York University.

He is the author of several books, including: Planning for An Aging Population; Business Entities: Start to Finish; Taxation of Divorce and Separation; Income Taxation of Estates and Trusts, Preparing the Audit-Proof Federal Estate Tax Return, Putting It Together: Planning Estates for $5 million and Less, Family Business Succession Planning, Business Acquisitions: Representing Buyers and Sellers in the Sale of a Business; Dynasty Trusts; Planning with Intentionally-Defective Grantor Trusts; The Federal Gift Tax: A Comprehensive Analysis; Charitable Remainder Trusts, Grantor Trust Planning: QPRTs, GRATs and SCINs, The Estate Planning Course, The Retirement Planning Course, Retirement Distributions: Estate and Tax Planning Strategies; The Estate Administration Course, Tax Strategies for Closely-Held Businesses, and Tort Litigation Settlements: Tax and Financial Issues.

Mr. Siegel has lectured extensively throughout the United States on tax, business and estate planning topics on behalf of numerous organizations, including National Law Foundation, AICPA, CCH, National Tax Institute, National Society of Accountants, and many others. He has served as an adjunct professor of law at Seton Hall and Rutgers University law schools.

The Siegel Group provides consulting services to accountants, attorneys, financial planners and life insurance professionals to assist them with the tax, estate and business planning and compliance issues confronting their clients. Based in Morristown, New Jersey, the Group has provided services throughout the United States. The Siegel Group does not sell any products. It is an entirely fee-based organization.

Contact the Siegel Group through its president, Steven G. Siegel, e-mail: [email protected].

The Siegel Group provides consulting services to accountants, attorneys, financial planners and life insurance professionals to assist them with the tax, estate and business planning and compliance issues confronting their clients. Based in Morristown, New Jersey, the Group has provided services throughout the United States. The Siegel Group does not sell any products. It is an entirely fee-based organization.

Contact the Siegel Group through its president, Steven G. Siegel, e-mail: [email protected].